Introduction

Most DTC founders treat refunds as a customer service headache. They're actually a cash flow crisis.

The NRF and Happy Returns report found $890 billion in merchandise was returned in 2024 alone - 16.9% of all retail sales. Chain Store Age reports global online return volumes jumped 18.1% in 2025. Every cash refund you issue doesn't just reverse a sale - it pulls working capital out of your business while you still absorb the shipping, processing, and restocking costs.

Store credit changes that equation. This guide walks you through exactly how to reduce your ecommerce refund rate's revenue impact, keep more money in your business, and turn refund moments into repeat purchases.

Why Your Refund Process Is Quietly Draining Your Business

Before You Begin: What You Need to Know

Before changing your refund policy, make sure you have these five things in place:

- Your current refund rate and monthly refund volume - know your baseline before you change anything

- A Shopify store - this guide is built for Shopify merchants

- A dedicated store credit tool - native Shopify store credit has real limitations; a platform like Rise.ai adds automation, bonus credit incentives, expiry controls, and redemption tracking

- A basic post-purchase email flow - Klaviyo integration recommended

- Your existing refund policy wording - you'll need to update it

- Difficulty level: Beginner to Intermediate. No coding required.

- Time to implement: 2-4 hours for policy and platform setup; 1-2 weeks to see your first data.

The True Financial Cost of Cash Refunds (It's More Than the Refund Amount)

Most merchants think a $100 refund costs them $100. It costs significantly more.

Here's what a single cash refund actually takes from your business:

- $100 - the refund itself, permanently removed from your revenue

- ~$3.20 - non-refundable payment processing fees (Shopify Payments and Stripe both confirm they don't return the original transaction fee)

- $8-12 - return shipping per item (UPCounting, 2025)

- $2-4 - restocking and storage

That's $116+ out the door on a single $100 order. Radial puts the average total return processing cost at $27 per $100 order - and only 30% of returned merchandise ever sells at full price again.

The real gut punch? That customer now has zero financial reason to come back. Store credit changes that equation.

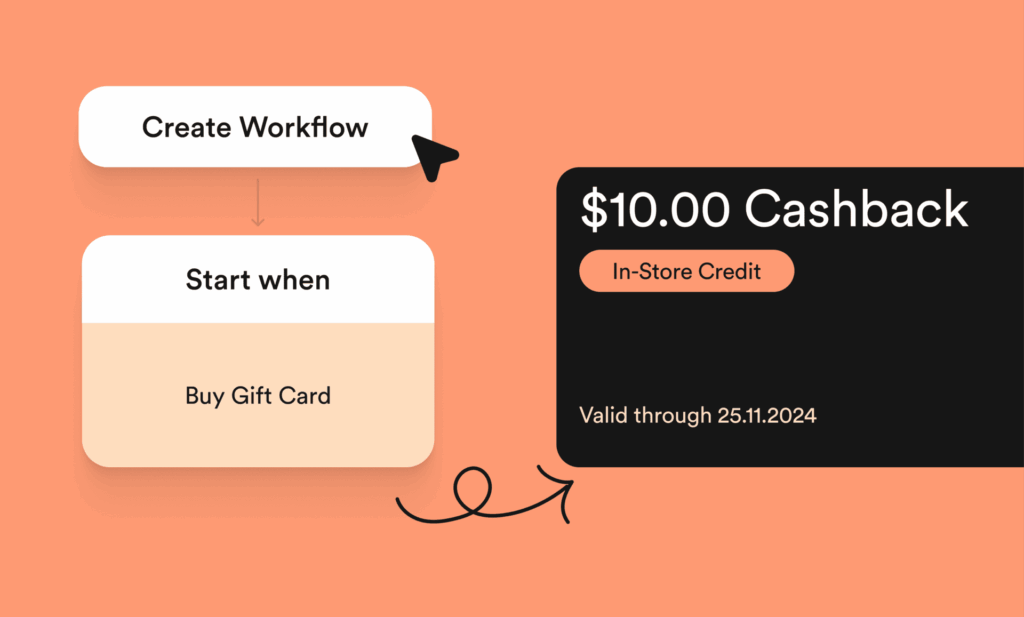

How a Store Credit Refund Policy Works: The Mechanics

The mechanics are simpler than you'd expect - and each step directly protects your bottom line. Here's exactly what changes when you replace a cash refund with store credit.

01

Customer Submits a Return or Refund Request

The customer contacts support or submits a request through your self-service returns portal. At this stage, capture three things: order value, return reason, and customer account status.

With Rise.ai, an approved return in Shopify automatically triggers a store credit workflow - no manual steps needed.

Don't skip the return reason. That data tells you exactly why customers are leaving - and where to fix it.

02

Issue Store Credit to the Customer's Account

Once approved, issue store credit equal to or slightly above the refund value. That small bonus is the difference-maker: eMarketer found that 54% of digital shoppers would choose store credit over cash if they received a small bonus, like $105 for a $100 return.

The credit appears as a visible balance in their account, redeemable at checkout. Always follow up with a branded notification email - customers who aren't reminded simply forget it's there.

03

Customer Redeems Credit on a Future Purchase

At checkout, the customer sees their available balance and applies it with one click - no codes, no friction. That simplicity matters. Complicated redemption kills follow-through.

When their new order exceeds the credit value, they pay the difference - and they almost always do. According to Rise.ai's Store Credit data, customers who used store credit spent over 300% more than the credit's value, with average order value increasing by 21%. A refund just became a revenue-generating return visit.

04

Track Redemption and Measure Revenue Retained

Issuing store credit without tracking redemption is like running ads without checking conversions - expensive and blind. You need three numbers: redemption rate, revenue retained vs. refunded, and AOV at redemption.

A healthy redemption rate sits between 60-80% when credit is properly communicated and incentivized. If yours falls short, the policy needs work - not the product.

The Financial Impact: What the Revenue Retention Math Actually Looks Like

Here's what the numbers look like for a Shopify merchant processing $10,000/month in refund requests.

Under a cash refund policy, all $10,000 walks out the door - plus roughly $320 in non-refunded processing fees. Under a store credit policy with a 60% conversion rate, $6,000 stays in your business. If 70% of that is redeemed, that's $4,200 in purchases. And because customers who redeem store credit spend over 300% of the credit value (Rise.ai merchant data), the actual revenue from those visits is far higher.

Over 12 months: $6,000/month retained x 12 = $72,000 that stays in your business.

Dottie Couture proved this at scale - issuing 10,000+ store credit refunds, cutting refund management costs by 42%, and watching their customer return rate climb to 53%.

> Run Your Own Numbers:

> Monthly Refund Volume x Store Credit Conversion Rate x Redemption Rate = Revenue Retained

How to Implement a Store Credit Refund Policy Without Damaging Customer Trust

The most common pushback we hear from merchants: won't customers revolt if they can't get cash back? The short answer is no - as long as you design the policy right.

Policy Design Decision 1: Offer Store Credit as the Default, Not the Only Option

There's a meaningful difference between forced and preferred - and your customers feel it immediately.

"Store credit only" policies generate negative reviews. "Store credit with a bonus" generates loyalty. According to eMarketer (December 2025), 54% of digital shoppers choose store credit over a cash refund when offered a small bonus - like $105 in credit for a $100 return.

Use this policy language as your template:

> "We offer two refund options: (A) Store credit for the full amount + 10% bonus - use it on anything in our store, no expiry pressure. (B) Cash refund to your original payment method."

Store credit becomes the reward. Cash becomes the fallback.

Policy Design Decision 2: Handle Edge Cases with a Cash Refund Safety Net

Use this simple decision rule: if the return is merchant error - defective item, wrong product, shipping damage - default to cash. If it's customer preference (wrong size, changed mind), offer store credit with a bonus.

Forcing store credit on a broken product is legally risky and practically counterproductive. Customers who feel trapped dispute the charge with their bank instead, and chargebacks cost far more than a straightforward refund. Your safety net isn't a loophole. It's chargeback prevention.

Policy Design Decision 3: Communicate the Policy Clearly Before Purchase

Surprise is the enemy of trust. Customers who already know about your store credit bonus before they need to return are far more likely to choose it willingly.

Embed your policy at four key moments:

- Product pages: "Easy returns: take store credit + 10% bonus, or a standard cash refund."

- Checkout: A one-line policy reminder in the order summary.

- Order confirmation email: Highlight the credit option alongside your return window.

- Shipping confirmation: Reiterate both return options before the package even arrives.

Proactive communication makes the policy feel like a perk, not a trap.

Turning Refund Recipients Into Repeat Buyers: The Retention Upside

A customer who just returned a product isn't a lost customer - they're a customer with money sitting in your store. A cash refund ends that relationship. Store credit keeps it alive and pulls them back.

The Post-Refund Re-Engagement Email Sequence

Three emails. That's all it takes to turn a refund into a repeat purchase.

- Email 1 - Day 0-1: "Your store credit is ready - here's what you've got." Confirm the credit amount, highlight any bonus, and include a 'Shop Now' CTA with 2-3 product recommendations. This email gets the highest open rate because customers are expecting it.

- Email 2 - Day 7-10 (if unredeemed): "Your $[X] credit is waiting - here are some new arrivals." Gentle reminder, fresh product suggestions, no pressure.

- Email 3 - Day 21-25 (if still unredeemed): "Don't let your store credit expire - use it before [date]." Clear expiry date, strong CTA, optional free shipping sweetener.

Rise.ai's Klaviyo integration triggers this entire sequence automatically based on credit issuance and redemption status - no manual tracking needed. Rise.ai merchants running this workflow have documented customer return rates surging to 53%.

Personalizing the Return Experience to Maximize Redemption

Generic follow-ups get ignored. Relevant ones get clicked.

Match your messaging to the return: if a customer sent back a dress over sizing, recommend items with detailed fit guides, not random bestsellers. Segment by credit balance, and adjust reminder frequency based on how often they browse.

Rise.ai's Klaviyo integration syncs store credit balance and redemption status in real time, so these flows build themselves.

The goal isn't to be pushy, it's to make coming back feel effortless. A customer who redeems credit and has a great experience is often more loyal than one who never had a problem at all.

How to Set Up Store Credit Refunds on Shopify with Rise.ai

No coding. No custom dev work. You're live in 2-4 hours.

- Install Rise.ai from the Shopify App Store

- Configure your refund workflow - set the trigger (return approved), credit amount, bonus percentage, and expiry conditions

- Customize your credit notification email with your brand colors, logo, and messaging

- Connect Klaviyo to trigger post-refund re-engagement flows based on credit issuance and redemption events

- Update your return policy page and checkout messaging to communicate the store credit option

- Go live and track redemption rates in Rise.ai Analytics

- What Rise.ai enables that native Shopify can't: bonus credit percentages, automated expiry controls, branded claim pages, Klaviyo-triggered sequences, and a unified dashboard showing revenue retained per refund.

Verifying Success: How to Know Your Store Credit Policy Is Working

Five numbers tell you whether your policy is retaining revenue or quietly leaking it:

- Store credit adoption rate - 40-60% of eligible refund customers choosing credit over cash within 60 days

- Redemption rate - 60-80% of issued credits redeemed with a solid re-engagement sequence

- Revenue retained - total credit issued minus any cash-equivalent losses

- AOV at redemption - Rise.ai merchant data shows a 21% AOV lift when customers return to spend their credit

- Repeat purchase rate among refund recipients vs. those who got cash back

Run a 30/60/90-day framework: Day 30 gives you adoption baseline data, Day 60 shows first redemptions and retained revenue, Day 90 gives you enough to sharpen your bonus credit percentage and email timing.

Troubleshooting: Common Issues and How to Fix Them

- Low adoption? Raise your bonus credit percentage, start at 5% and test 10%, and confirm customers can actually see the offer at the point of refund.

- Credits issued but not redeemed? Audit your email sequence first. If open rates are low, tighten the expiry window to 30-60 days to create urgency without feeling punitive.

- Customer complaints? Complaints almost always mean surprise. Check whether your policy is visible pre-purchase and whether defective products are getting cash refunds, not credit.

- Tracking gaps? Pair Rise.ai Analytics with your Klaviyo data for full-funnel attribution on every credit redemption.

Next Steps: Expanding Store Credit Beyond Refunds

Refunds are just the entry point. Store credit can also power loyalty rewards for repeat purchases, win-back campaigns for lapsed customers, referral incentives, and cart abandonment recovery, all from one platform instead of four disconnected tools.

That's exactly what Rise.ai is built for. Over 5,000 brands already use it to automate store credit across every customer touchpoint.

If refunds are draining your cash flow right now, the fastest fix is to start issuing store credit instead. Rise.ai makes it automatic. Start your free trial today.

Conclusion

Store credit won't eliminate returns, but it fundamentally changes what a return costs you. Instead of losing revenue permanently, you retain it, re-engage the customer, and create a second purchase opportunity - all without adding friction to your refund process. The mechanics are straightforward, the setup is fast, and the financial case is clear.

Ready to Turn Refunds Into Repeat Revenue?

Rise.ai's Store Credit Accounts automate the entire refund-to-credit workflow on Shopify - so you keep revenue in your business without lifting a finger. Join 5,000+ brands already doing it.

FAQs

Is it legal to offer store credit instead of a cash refund?

In most jurisdictions, yes—but with important caveats. In the US, there is no federal law requiring cash refunds; return policies are set by the retailer. However, some states (like California and New York) have specific rules about store credit policies, particularly around expiry dates and disclosure requirements. For defective products or items that don’t match their description, consumer protection laws in many regions require a full cash refund option. Always consult local regulations and ensure your policy is clearly disclosed before purchase. The safest approach is to offer store credit as the incentivized default while keeping a cash refund option available—this protects you legally and builds customer trust.

Will customers leave negative reviews if I switch to a store credit refund policy?

Only if they feel surprised or forced. The data shows that when store credit is offered with a bonus (e.g., $110 credit for a $100 return) and communicated transparently before purchase, 54% of digital shoppers actively prefer it over a cash refund (eMarketer, December 2025). Negative reviews typically come from two scenarios: (1) customers who were not informed of the policy before purchase, and (2) customers with defective products who are denied a cash refund. Solve both by communicating the policy clearly at checkout and always offering cash refunds for merchant-error returns. Brands using Rise.ai’s store credit refund system—like Dottie Couture, which issued 10,000+ store credit refunds—report reduced operational costs without documented increases in negative sentiment.

What percentage of customers actually redeem store credit after a refund?

Redemption rates vary based on how well the credit is communicated and incentivized, but well-implemented store credit programs typically see 60–80% redemption rates. The key drivers of high redemption are: (1) a bonus credit amount that makes the credit feel more valuable than cash, (2) a clear and timely notification email sent immediately after credit issuance, (3) a follow-up reminder sequence before the credit expires, and (4) relevant product recommendations that make it easy for the customer to find something they want. Rise.ai merchant data shows that customers who redeem store credit spend over 300% more than the credit’s face value, meaning the redemption event itself generates significant incremental revenue.

How do I set up store credit refunds on Shopify?

Shopify has native store credit functionality, but it has significant limitations—it doesn’t support bonus credit percentages, automated expiry controls, or triggered email sequences based on credit events. For a fully automated store credit refund workflow, most Shopify merchants use a dedicated platform like Rise.ai. The setup process involves: (1) installing Rise.ai from the Shopify App Store, (2) configuring a workflow that triggers store credit issuance when a return is approved, (3) setting your bonus credit percentage and expiry terms, (4) customizing the customer notification email, and (5) connecting to Klaviyo for automated re-engagement sequences. The entire setup takes 2–4 hours and requires no coding.

How much bonus credit should I offer to incentivize customers to choose store credit over cash?

The sweet spot for most ecommerce brands is 5–15% above the refund value. eMarketer research (December 2025) found that a modest bonus—like $105 in credit for a $100 return—is enough to shift 54% of digital shoppers toward store credit. Start with 10% and measure your adoption rate over 30 days. If adoption is below 40%, increase to 15%. If adoption is already above 60%, you may be able to reduce to 5% and maintain strong conversion while improving your margin on the bonus. The bonus credit is a cost, but it’s significantly cheaper than the alternative: losing the full refund amount plus processing fees, return shipping, and restocking costs.

Does offering store credit instead of cash refunds hurt customer lifetime value?

The evidence suggests the opposite. Customers who receive store credit and redeem it are more likely to make repeat purchases than customers who receive cash refunds and have no financial reason to return. Rise.ai’s merchant data shows that customers who use store credit spend over 300% more than the credit’s value and that customer return rates surge to 53% among store credit recipients. The key is execution: store credit that is easy to redeem, well-communicated, and paired with relevant product recommendations converts a potentially negative refund experience into a positive re-engagement moment. Brands using store credit as a retention tool—rather than a restriction—consistently report higher repeat purchase rates and customer lifetime value.